Better Mortgage aims to reduce the time it takes for our customers to refinance. In this article, we share the experiences of two real customers who closed their loans in under 21 days and give you tips on how you might be able to speed up your refinance process.

If you go to a traditional lender, they'll tell you that refinancing a home takes around 5–7 weeks from application to close. But it is possible to close much faster than that—even with the prospect of delays from appraisals, inspections, and other third parties. In fact, our simple, online process helps our average customer close 10 days faster than the industry average*.

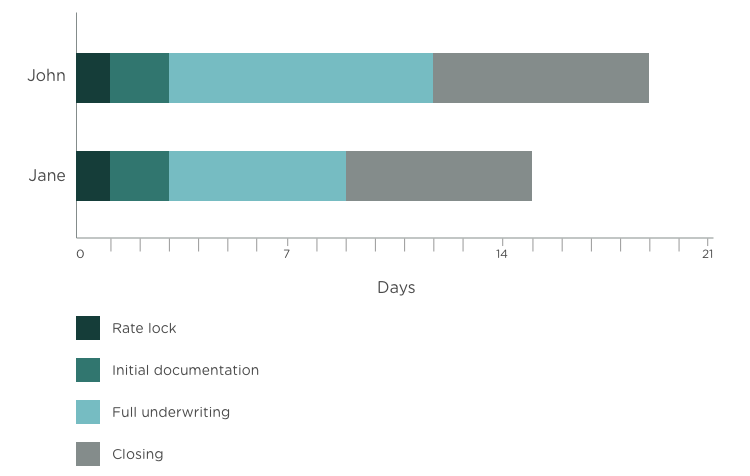

I'd like to share the experiences of two of my real borrowers (we’ll call them John and Jane to protect their privacy) who coincidentally closed on the same day in February 2017—both in less than 3 weeks. That’s not only much faster than the industry standard, but faster than the average Better Mortgage customer as well.

John and Jane's actual loan timelines

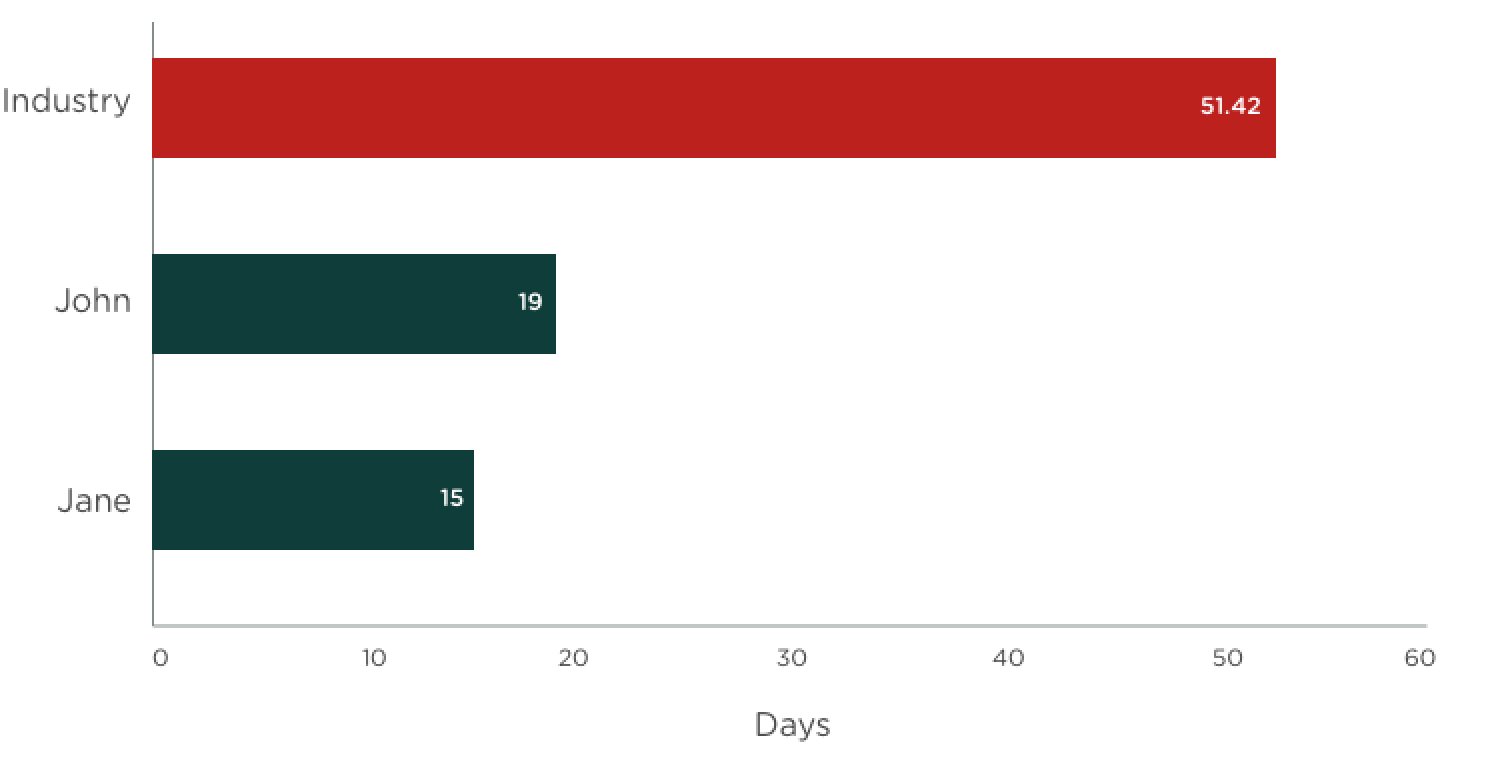

Compare these examples to the industry average of 51.42 days1 average application-to-close and you'll see how much faster Better Mortgage can be!

Industry average application-to-close compared to John and Jane's loans

As you can see from the timelines, the Better mortgage process is fast! Our team analyzed the reasons behind the successes of these case studies. While Better Mortgage’s innovative technology was a key factor, the most important component was actually the borrower.

3 tips for how you can drive the process

Our team came up with 3 tips for current and future borrowers who are ready to get a loan in 3 weeks or less.

1. Be prepared with the documents you know you’ll need

While every loan requires slightly different documentation based on the borrower’s financial details, there are some standard financial documents that every loan will require, such as:

- 2 years of W2 forms and personal tax returns

- The most recent 2 months of paystubs and bank statements (from all accounts)

- Updated insurance policies

Of course, since we’re a digital lender, we ask you to provide these documents electronically. If you round up these documents in PDF form, you’ll have a head start.

Both John and Jane had all the required documents ready, uploading the initial income and asset documents within 24 hours of locking their rates.

2. Be proactive when it comes to outstanding tasks

The most important thing you can do is respond quickly to any questions and documentation requests. The fastest borrowers, like John and Jane, respond to requests within hours and never wait for a reminder to complete outstanding tasks.

In John’s case, just a couple days before closing we identified a need to obtain an additional statement from a previous lender. When we told John of the need, he immediately called the lender to get the statement. His quick action ensured we could close the loan on schedule.

3. Be communicative with your lender at every step

If anything is unclear or requires additional discussion — email, call, or send us a message. We encourage questions. A big part of our role is to educate and help you make informed decisions.

Even though John and Jane's loans took only 3 weeks, our loan team had the pleasure of getting to know them well. John in particular gave day-to-day updates on his progress, which was fantastic.

“Our goal is to get our borrowers to the closing table ASAP. Good communication is always a key to making that happen.”

Sathi Roy, Mortgage Expert

Get started

Every situation is different, but if you’re prepared, proactive, and communicative, you may be able to speed up the time it takes to refinance. If you’re wondering whether now is a good time to refinance, try out our handy refinance calculator to see how much you could save. And when you’re ready to go, you can get a rate quote in less than a minute. With Better Mortgage, refinance in weeks, not months.

EllieMae Origination Insight Report, February 2017 ↩